For a world that has spent the better part of three years bracing for economic slowdowns, the latest numbers feel almost surreal. Growth is not just holding—it’s accelerating in pockets that few expected. Factories in Asia are humming louder than forecast, U.S. consumer spending continues to defy gravity, and even parts of Europe—despite its bruising energy story—are reporting stronger-than-expected resilience. The phrase “global recession” that haunted boardrooms and headlines not so long ago now sounds oddly premature.

But here’s the catch: every silver lining has a storm cloud attached.

A Recovery That Refuses to Fade

The International Monetary Fund and other watchful institutions had penciled in a soft year. Trade wars, supply chain bottlenecks, energy crunches, stubborn inflation—take your pick; the reasons to expect weaker growth were abundant. Yet, against this backdrop, global GDP has outpaced most estimates. The service sector boom, particularly in travel and digital industries, has been a quiet powerhouse. Airlines report record bookings, streaming platforms keep swelling, and luxury brands—from Milan to Shanghai—say their tills are ringing again.

Emerging markets have surprised too. India continues to clock growth rates closer to startup valuations than sober economies. Parts of Southeast Asia are benefiting from companies “China-plus-one” strategies, redirecting supply chains in search of resilience. Even in Africa, where investment cycles often move at a slower pace, renewable energy and fintech corridors are showing momentum.

Why the Good News Feels Fragile

Still, optimism has limits. Inflation, while cooling in some geographies, is far from conquered. Central banks are playing a delicate game—tighten too much and risk choking growth, loosen too soon and reignite price surges. The U.S. Federal Reserve’s recent pause was met with cheers, but traders know the celebration can turn on a dime if data swings.

There’s also the matter of debt. Governments borrowed heavily during the pandemic years, and repayment schedules are looming. Developing nations, in particular, face the dual challenge of managing external debts while funding infrastructure and social programs. The phrase “debt distress” is quietly working its way back into economic briefings.

Meanwhile, trade tensions haven’t disappeared—they’ve simply shape-shifted. Tariffs may no longer dominate headlines, but protectionist policies, export controls, and national security-driven restrictions are multiplying. Add in the simmering geopolitical conflicts—from Eastern Europe to the South China Sea—and the global economy looks more like a tightrope act than a victory lap.

The Human Pulse Behind the Numbers

For households, the contradiction is palpable. Yes, jobs are plentiful in many economies, but wages still trail the rising costs of living. Mortgage payments are heavier, groceries sting more, and energy bills keep families on edge. In conversations across cities—from New York to Nairobi—the refrain is similar: the economy may be “growing,” but people feel like they’re running harder just to stay in place.

Corporate leaders echo this unease. Tech giants that once scaled at breakneck speed are more cautious with hiring. Manufacturing CEOs worry about input costs. Even the booming AI sector, the darling of investors, is facing its own questions: can demand keep pace with the hype, or will the bubble deflate?

Growth Now, Uncertainty Next

The paradox of today’s global economy is that the strength of the present may be sowing the seeds of tomorrow’s slowdown. Strong consumer demand keeps inflationary embers alive. Resilient labor markets pressure central banks to keep policy tight. And markets, ever forward-looking, are already pricing in the possibility that this growth cycle may not have long legs.

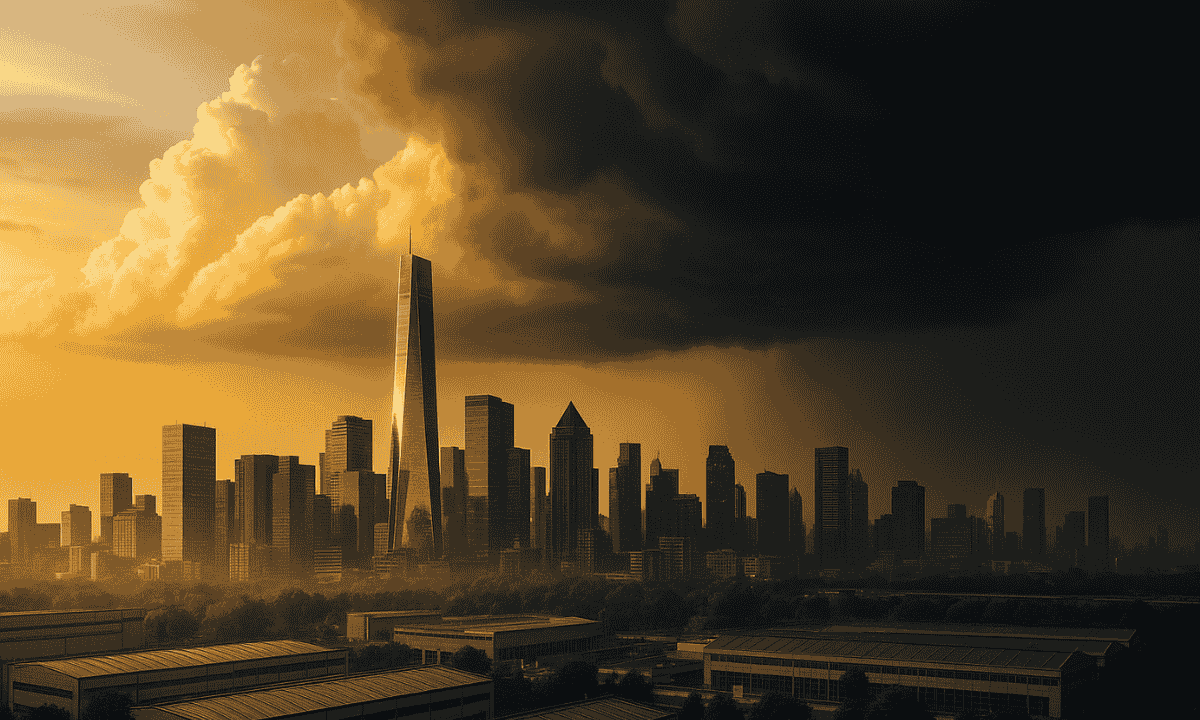

So, while the numbers tell a story of resilience, the sentiment underneath is more complex: cautious, restless, and occasionally skeptical. The world has learned—sometimes brutally—that good times in a globalized economy can shift overnight.

For now, the music is still playing. Factories are running, planes are full, and stock indices look healthier than feared. But the dance floor feels crowded, and somewhere in the background, storm clouds are gathering. The question isn’t whether they’ll arrive—it’s how hard they’ll hit when they finally do.